Laser machines, treatment beds, staffing, and marketing — costs add up fast, especially if you’re just starting or expanding services.

Unless you’ve major savings or a private investor, you’ll likely need financing solutions to get things moving.

But navigating loans can be tricky. Many owners face strict requirements, cash flow challenges, and confusing funding options. It’s easy to feel overwhelmed.

That’s where this guide comes in. We’ll walk you through exactly how to:

👉 Figure out how much to borrow

👉 Choose the right loan type

👉 Strengthen your loan application and avoid common pitfalls

Let’s break it all down and help you get funded💰

Understanding your med spa’s financial needs before applying for a loan

This info will greatly impact the type of loan you need, so let’s see what that entails.

Assessing startup vs. Expansion costs

Med spas require a significant upfront investment, whether you’re just starting your aesthetic business or scaling to expand it.

Typical initial one-time med spa startup costs

Expansion costs

Company setup

New treatment rooms

Lease deposits and renovations

Extra equipment such as laser machines or body sculpting tools

Furnishings

Extra staff

Equipment

More inventory

Inventory

Marketing

Staff payroll

/

Software

/

Licenses and permits

/

Insurance

/

The costs for all of these mentioned depend on many factors, such as location, whether you’ll lease or rent, the type of equipment you need, how much staff you initially intend to hire, etc.

Full-scale setup (brand-new space + high-end equipment): $400,000–$600,000+

Keep in mind, these are ballpark figures — your actual startup costs will vary based on your vision, goals, and local market.

Calculating how much you need to borrow

You’ve mapped out your expenses and how much you need to borrow. Now it’s time to tally them up. Let’s imagine your costs break down like this:

Lease deposit and renovation = $30,000

Equipment = $50,000

Software and licenses = $5,000

Staff salaries (for the first three months) = $45,000

etc…

Total estimated loan amount = $130,000

You can use this formula to see if your loan is pulling its weight:

(Revenue Increase – Loan Payment) ÷ Loan Payment

If the result is:

1 – You’re earning 100% more than you’re paying

0 – You’re breaking even

Negative – The loan is costing more than it’s making

For example:

If you calculated you’d be brining in $9,000 of revenue per month and your loan payment is $3,500 per month: (9,000 – 3,500) ÷ 3,500 = 1.57

To represent this as a percentage, multiply the result by 100 — so in this case, you’d be earning 157% more than you’re paying.

You can also use our free excel spreadsheet to forecast your cash flow, input your bank balance, predicted expenditures, and anticipated sales. It can show you how your med spa will perform in the next 12 months.

There’s no one-size-fits-all here — the best option depends on:

Your credit

How quickly do you need the funds

What do you plan to spend the money on

Here’s a breakdown of the most common loan types, what they’re good for, and what to watch out for.

Small business administration (SBA) loans: Low-interest & government-backed

SBA loans are best for established med spa owners with good credit histories.

👍 Pros

⚠️ Cons

Government-backed

Tough qualification criteria

Lower interest rates

Long approval process

Longer repayment terms

/

Higher borrowing limits

/

In short, the qualification criteria for these loans are stricter, and the process for approval is lengthy.

Traditional bank loans: High approval standards, but stability

Conventional bank loans are best for med spas with strong revenue and excellent financial records.

👍 Pros

⚠️ Cons

Stable

Requires great credit

Competitive interest rate

Lots of documentation

📌Bottom line: Strong financials and patience with paperwork are key to securing these loans.

Business lines of credit: Flexible funding for ongoing expenses

If your med spa business needs a loan credit for bulk inventory or surprise costs, business lines of credit are your best option.

👍 Pros

⚠️ Cons

You only pay interest on what you use

Interest rates can fluctuate

Have revolving access to funds

May need collateral

These loans are ideal for short-term needs, just watch for changing rates and collateral requirements.

Equipment financing: Ideal for med spa-specific investments

Equipment financing loans are best for med spas looking to buy new equipment, such as laser machines, cryo devices, or therapy tables.

👍 Pros

⚠️ Cons

The equipment is the collateral

Interest rates can be higher

They’re often easy to qualify for

/

Overall, they’re easy to qualify for, but you should expect slightly higher interest.

Alternative financing: Merchant cash advances & revenue-based loans

They are best for med spas with strong credit card sales but weak credit history.

👍 Pros

⚠️ Cons

Fast funding

Daily repayment withdrawals

No collateral needed

High interest fees

This loan is easy to get but hard to pay off — best for short-term fixes, not big investments.

How to qualify for a business loan for your med spa

Before a lender says yes, they want to see that you’re serious — and that your business is in good shape. The better prepared you are, the better your odds of getting approved (and scoring better rates while you’re at it).

Here’s how to set yourself up for success.

Improving your credit score & financial profile

Your credit score matters.

Whether it’s your personal credit or your business’s, lenders will comb through your financial history. But it’s not just about the number; they’re also looking at things like:

Credit history: Have you paid your bills on time? Do you have a track record of responsible borrowing?

Revenue stability: How consistent is your monthly income? Is your business generating reliable cash flow

Debt-to-income ratio: How much debt are you already carrying compared to how much you earn?

To improve your credit profile, you can:

✔️Check your credit reports for errors (you’d be surprised how common they are)

✔️Pay down existing debt

✔️Set up automatic payments so you never miss a due date

✔️If you don’t have business credit yet, start building it with a business credit card

Lenders notice when you’ve done the work, so start early.

Preparing a strong business plan for loan approval

A solid business plan isn’t just for impressing investors. Lenders want to see one, too.

They’re looking for proof that you’ve done your homework and have a clear plan to repay what you borrow.

📋 Your loan business plan should include:

Market analysis: Who are your clients? What makes your med spa stand out?

Detailed revenue projections: Monthly income goals, pricing strategy, seasonality

Expense forecasts: Rent, payroll, product costs, etc.

A clear repayment strategy: How will the loan help you grow? How will you pay it back?

Show lenders you’re not just asking for money — you’ve got a plan to make it work.

Gathering the required loan documentation

Loan paperwork can be daunting, but unfortunately, most lenders will ask for a set of the standard documents, such as:

✅Gather personal and business tax returns for at least the two last years

✅Profit and loss statements

✅Balance sheets

✅Business licenses and registrations

✅Bank statements

✅Equipment invoices

✅Collateral documentation (if applicable)

Having them ready can speed things up a lot, so you need to get ahead with a checklist.

Choosing the right lender for your med spa business loan

Finding the right lender is more than just comparing rates. They help you get favorable terms for your loan and reach your goals.

Here’s how to size up your options.

Comparing banks, credit unions, and online lenders

Depending on your business’s stage and financials, each lender type comes with its pros and cons:

Banks

Credit unions

Online lenders

✅ Great for long-term financing

✅ More flexible than banks

✅ Faster approval (sometimes in 24–48 hours)

✅ Lower interest rates

✅ Potentially more lenient underwriting

✅ Easier application process

🚫 Slower loan program process

🚫 May require membership or be limited by location

🚫 Higher interest rates

📌Bottom line: Banks are solid but slow, credit unions are flexible, and online lenders are fast but may cost more.

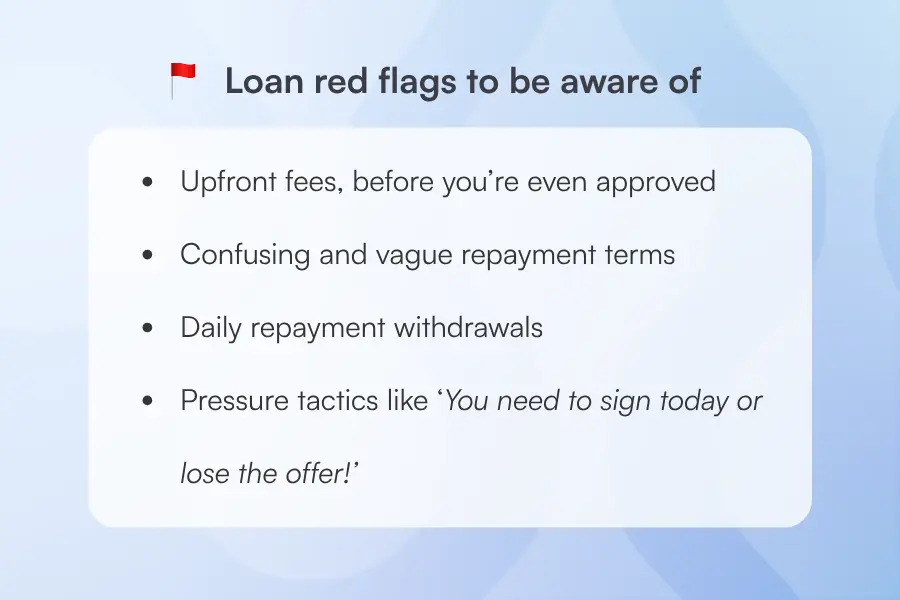

Avoiding predatory lenders & high-fee loans

When you need funding fast, getting caught in a trap is easy. Some lenders bank on that, which is why you must watch out for red flags like:

Upfront fees and manufactured urgency to sign are classic warning signs that a lender might be more interested in trapping you than genuinely helping. Plus, when payment terms are vague or required too often it means you’ll most likely end up paying far more than you planned.

💡If it feels off, trust your gut. Check their reviews, BBB rating, and whether they’re licensed to lend in your state.

If you don’t like what you’re seeing, other ethical alternatives might be a better fit, such as:

You lose nothing by exploring these loan avenues. They’re just more options to consider as secure and transparent ways to get the funding you need.

Tips for increasing your chances of loan approval

Getting a business loan doesn’t have to feel like a puzzle. A few simple steps can make all the difference in getting approved.

Here’s how to get started on the right foot.

Strengthening your financial statements before applying

Your financial statements are your business’s report card. That’s why you should do payment reconciliation — compare what’s in your company’s internal financial records to other records, such as bank statements or credit card statements.

To strengthen you financial statements⬇️

📊 Keep your cash flow visible and tidy: Lenders want to see steady money coming in and out, not a mystery mess.

💳 Pay down debts where you can: Because less debt means you’re less risky

🧾 Keep your revenue and expenses well documented and up to date

Considering a co-signer or collateral to improve loan terms

If your credit or financial history isn’t quite where you want it, don’t stress. What you can do is:

🤝 Bring in a co-signer: Someone with strong credit who agrees to take responsibility if you can’t pay — think a trusted partner or family member.

🏠 Put up collateral: An asset you pledge as security could be your med spa equipment, property, or inventory.

Both can help you snag better rates or loan amounts, but be sure everyone’s on the same page before signing anything.

Secure the right financing for your med spa & grow your business with Pabau

A business loan can open doors… or lead to chaos if you’re not careful about using it wisely.

To use it wisely, you need the right tools by your side, and that’s where Pabau comes in handy.

It’s an all–in–one practice management software that helps med spas manage booking and scheduling, patient record management, marketing, payment processing, and more — all in one platform.